Credit card surcharges are popping up at more merchants

More and more Long Island merchants are dinging shoppers with fees for using credit cards, and many of them are doing it in a way that breaks the law.

The surcharges, often running 3% to 4% of the bill, are usually listed on receipts as a "noncash adjustment" or "convenience" fee.

These so-called swipe fees are becoming common at delis and restaurants in the region. But Long Islanders are also seeing the charges when visiting hair salons, going to the doctor, getting their cars repaired and even arranging a cremation.

While it is legal for businesses to pass on credit card processing fees to customers, the practice many stores use — simply posting a small sign at the register informing shoppers they will pay extra for using plastic — is not.

Under New York State law, stores and restaurants must post the higher prices charged to credit card users on shelves, price tags and menus, the state Division of Consumer Protection told Newsday. They may also list the lower cash prices, just as gas stations post cash and credit prices. But they may not surprise customers at the register with the higher credit price.

Sticking customers with swipe fees without proper notice seems to be the norm at delis and convenience shops on the Island. Eight of 10 establishments along Route 110 passed on processing fees ranging from about 3% to 4% when Newsday made purchases this month. Just one, Roast Sandwich House in Melville, included the higher credit card prices on its menu. Most of the others had small signs near the register alerting customers that the posted prices were contingent upon using cash.

A growing number of New Yorkers are concerned about the fees: Complaints about credit card surcharges filed with regulators grew from three in 2020 to 138 in 2021 and 146 so far in 2022, according to the state Division of Consumer Protection, which mediates disputes and educates consumers and businesses on the law. The division said enforcement falls to the attorney general's office, which investigates complaints on surcharges and encourages concerned consumers to submit them.

But many merchants told Newsday they believed they were complying with the law by informing customers with a sign at the register or a note on the menu. Even officials at some payment processing firms, which advise business owners on how to pass on the fees, said they thought the signs were sufficient. Legal experts said their confusion is justified.

Businesses have long been burdened by credit card processing fees, which typically top out at 4% of the transaction, payment processing firms said. Court decisions in the past decade paved the way for companies to pass them on to customers through surcharges, lawyers said.

Banks and credit card networks in the United States often prohibited retailers from charging customers for using cards, but this changed in 2013 as part of a legal settlement Visa and Mastercard reached with merchants, according to the Tayne Law Group, a debt relief firm based in Melville.

In New York, section 518 of the state’s General Business Law allowed companies to raise rates for customers paying with cards, but the 1984-era measure wasn’t written clearly, said Jay Hack, a partner at Manhattan law firm Gallet Dreyer & Berkey who focuses on banking and financial institutions. Several courts examined the measure, including the U.S. Supreme Court and U.S. District Court for the Southern District of New York, which noted the language is so vague that “Alice in Wonderland has nothing on section 518.”

Then in 2018, a majority of the state Court of Appeals judges decided the state law is fulfilled "if and only if the merchant posts the total dollars-and-cents price charged to credit card users," which alleviates "concerns about luring or misleading customers by use of a low price available only for cash purchases."

Businesses can be fined up to $500 for each violation, asked to refund the amount not properly disclosed and potentially charged with a criminal misdemeanor — although courts are unlikely to impose such a serious penalty, according to Hack.

Most business owners that spoke with Newsday said they didn't realize that they were skirting the law by listing cash prices and posting signs stating that credit card users would be charged more.

"It gets kind of challenging," said Tayne Law Group founder Leslie Tayne, who noted that merchants are also dealing with credit card network and issuer rules that may forbid surcharges, but allow them to pass off the cost if it's described as a convenience fee. "They all have to be disclosed no matter what. There can't be any surprises."

Many companies on the Island, particularly mom-and-pop operations, stopped absorbing swipe fees during the COVID-19 era, when running a business became more challenging, payment processing firms said.

Early in the pandemic, more customers avoided cash and used cards, which made the swipe fees a bigger burden, merchants said. And now, with skyrocketing inflation pushing up their other costs, even more businesses are transferring processing fees to consumers because they're one of the few expenses that can be curbed, payment processors said.

UpNexa, a Holbrook firm that processes payments for merchants, has seen a 60% increase in the number of companies passing on the fees since the pandemic began, said chief operating officer Jazzel Riquelmy.

"Before, it was like the deli and the bagel shops that were really interested in doing it,” said Riquelmy, of Mount Sinai. “We’ve seen a big influx from those with larger tickets: the restaurants, the medi spas — even down to churches and [private] schools.”

Credit card transactions come with at least two fees. A fee averaging 1.3% to 3.3% of the transaction value is charged by the bank or institution that issued the credit card; and an average of 5 to 10 cents per transaction is collected by Visa, MasterCard or other networks used to transfer the money, according to The Motley Fool, a personal finance-focused publication.

Businesses often hire merchant processing firms to ensure everyone involved gets the proper fee — and their services also cost money, said Desh Singh, who launched CardEvo Inc., a Melville-based payment processing company, with his brother PJ Singh about four years ago.

“I’d say there’s five to 10 companies that are being paid out all at the same time for each transaction,” Singh said.

He estimated that before passing on the cost to customers, his Long Island clients paid an average of $1,050 a month in processing fees — an expense that has grown with the proliferation of credit cards that give people travel points, cash back or other rewards for charging purchases. These types of cards tend to have higher processing rates, according to The Motley Fool.

American businesses paid $105.2 billion in fees last year to accept credit card payments, according to the Nilson Report, which publishes updates on the card and mobile payment industry. That's 25% more than firms spent in 2020 and 50.8% more than they paid five years before that, Nilson said.

Merchants must also pay to accept payments via debit card, but the fees are lower because the federal government has capped them for about a decade. Still, many businesses subject debit and credit card users to the same fees because distinguishing between the two and treating them differently would be too complicated, Tayne said.

The industry draws from fee revenue to combat fraud and ensure networks can safely and quickly transfer money, according to the Electronic Payments Coalition, a trade group for credit card issuers and networks. The group's chairman Jeff Tassey said credit card rewards programs induce enough spending to benefit everyone, including small businesses.

Swipe fees became too much for Capo Ristorante in Franklin Square during the pandemic, owner Paul Capoziello said. Processing costs were sometimes more than the restaurant's rent, he said. Demand for delivery skyrocketed and nearly all customers paid with plastic; today, about 87% do, Capoziello estimated.

A fire destroyed Capo's prior location and Capoziello tacked a 4% fee onto credit card bills when he reopened the restaurant in Franklin Square last year. Keeping a less expensive cash option for those on a budget seemed better than raising his prices across the board, Capoziello said. He said the shift went over fine with customers.

“Uber Eats, DoorDash — people choose to get deliveries of food from them, and they pay 30% more to get it delivered,” said Capoziello, of Franklin Square. “If they come in and get it or they’re ordering it from me, what’s another 4%?”

Melville Deli on Route 110 shut for two months in the early days of COVID-19 and then spent six months recovering from the closure, co-owner Simaan Gaffary said. With attendance at nearby offices down and food prices up, instituting a 3.5% surcharge on cards has helped the business save about $2,500 to $3,000 a month in fees, he said.

"That made the difference," said Gaffary, of Islip. "Before that we weren't making anything."

Signs on the deli's refrigerated displays announce a special offer of $12.95 for premade heros or $6.99 for half a sandwich — both of which are only relevant to customers with cash. On the front of the cash register, one sign notes the advertised prices reflect a cash discount and a second handwritten note says there will be "a 3.50% immediate discount on service charge" for those paying with cash or a gift card. Gaffary said he believed the setup met government standards, noting that it was approved by his merchant processor.

At Bay Deli in Halesite, owner Conrad Pohlmann instituted a card surcharge when a customer with payment processing experience suggested he do so. Pohlmann posted a sign near the register alerting customers that the advertised prices factor in a 3.5% discount for using cash. He now pays about $2,000 a year in processing costs, compared with $8,000, Pohlmann said.

"It's well worth it," said Pohlmann, who noted nobody has suggested his system doesn't meet state standards.

At Signature Styles hair salon in Patchogue, owner Jean Bieselin is weighing whether to start splitting the processing payments with customers in 2023. The swipe fees she pays rose earlier this year, which helped push the salon’s monthly processing tab up to about $500, Bieselin said.

Her salon is facing other challenges, including having to buy products from Amazon because cheaper alternatives aren't available from wholesalers.

“I took on a responsibility to pay a certain amount,” said Bieselin, of Patchogue. “It’s getting astronomical."

For small businesses, credit card processing fees have become a bigger concern under current economic conditions, Singh said. Firms are grappling with higher supply and labor costs and consumers tightening their budgets, he said. Many mom-and-pop enterprises can’t survive without cutting costs — and passing on these fees may be one of the few options at their disposal.

“They’re having to do this out of necessity to stay afloat," Singh said.

Nationwide, about 23% of small businesses use credit card surcharges, adding an average of 2.3% of the transaction value, according to a survey conducted by The Strawhecker Group, a payment consulting firm.

More Long Island firms are adopting this strategy as well, Singh said. Early in the pandemic, just a fraction of businesses working with CardEvo had consumers cover credit card fees, Singh said. Now nearly 90% of new clients opt for that model, he said.

Long Islanders have taken notice, with some saying they try to bring cash when eating out or running errands.

Jordan Hoffman, of Babylon, said he routinely informs businesses that their prices aren't properly displayed. Managers and owners respond that their system was OKd by a payment processor, he said.

If businesses give him a hard time, Hoffman notifies the attorney general's office. He's filed roughly 15 complaints with the office and seen two or three businesses reform their ways, said Hoffman, a real estate attorney.

Sharon Abrams, a retiree in Nassau County, said surcharges can be particularly shocking on big expenses.

Her husband died this summer, and Abrams worked with a funeral home to fulfill his request to have his body cremated. She was surprised to hear that using a card to cover the more than $1,375 service would come with a nearly $50 "convenience" fee. Abrams said she had no choice but to agree to the arrangement.

“I didn’t have liquid cash,” she said.

"When it happens in restaurants … most people are just like: eh, it stinks,” Abrams added. “When it is for something substantial, it can make a difference.”

Surcharges — even for smaller purchases — bother Debbie Jansen, of Great Neck.

She sympathizes with businesses that suffered during lockdowns, but noted that customers have also weathered tough spells.

“Many of us were unemployed for a long, long time and are thrilled to even be able to go out to eat,” said Jansen, who lost two jobs during the pandemic and works as an administrative receptionist.

More and more Long Island merchants are dinging shoppers with fees for using credit cards, and many of them are doing it in a way that breaks the law.

The surcharges, often running 3% to 4% of the bill, are usually listed on receipts as a "noncash adjustment" or "convenience" fee.

These so-called swipe fees are becoming common at delis and restaurants in the region. But Long Islanders are also seeing the charges when visiting hair salons, going to the doctor, getting their cars repaired and even arranging a cremation.

While it is legal for businesses to pass on credit card processing fees to customers, the practice many stores use — simply posting a small sign at the register informing shoppers they will pay extra for using plastic — is not.

What to know

- Credit card processing costs are being passed on to consumers through surcharges at more and more LI stores and restaurants.

- The state allows merchants to charge higher rates to those paying with plastic.

- Dollar-and-cent prices for credit cards must be posted; cash prices may also be displayed.

- Request assistance from the state Division of Consumer Protection at dos.ny.gov/consumer-protection.

- Report violations to the state Attorney General’s office at on.ny.gov/3VCSUm6.

Under New York State law, stores and restaurants must post the higher prices charged to credit card users on shelves, price tags and menus, the state Division of Consumer Protection told Newsday. They may also list the lower cash prices, just as gas stations post cash and credit prices. But they may not surprise customers at the register with the higher credit price.

Sticking customers with swipe fees without proper notice seems to be the norm at delis and convenience shops on the Island. Eight of 10 establishments along Route 110 passed on processing fees ranging from about 3% to 4% when Newsday made purchases this month. Just one, Roast Sandwich House in Melville, included the higher credit card prices on its menu. Most of the others had small signs near the register alerting customers that the posted prices were contingent upon using cash.

A growing number of New Yorkers are concerned about the fees: Complaints about credit card surcharges filed with regulators grew from three in 2020 to 138 in 2021 and 146 so far in 2022, according to the state Division of Consumer Protection, which mediates disputes and educates consumers and businesses on the law. The division said enforcement falls to the attorney general's office, which investigates complaints on surcharges and encourages concerned consumers to submit them.

But many merchants told Newsday they believed they were complying with the law by informing customers with a sign at the register or a note on the menu. Even officials at some payment processing firms, which advise business owners on how to pass on the fees, said they thought the signs were sufficient. Legal experts said their confusion is justified.

Tangled legal web

Businesses have long been burdened by credit card processing fees, which typically top out at 4% of the transaction, payment processing firms said. Court decisions in the past decade paved the way for companies to pass them on to customers through surcharges, lawyers said.

Banks and credit card networks in the United States often prohibited retailers from charging customers for using cards, but this changed in 2013 as part of a legal settlement Visa and Mastercard reached with merchants, according to the Tayne Law Group, a debt relief firm based in Melville.

In New York, section 518 of the state’s General Business Law allowed companies to raise rates for customers paying with cards, but the 1984-era measure wasn’t written clearly, said Jay Hack, a partner at Manhattan law firm Gallet Dreyer & Berkey who focuses on banking and financial institutions. Several courts examined the measure, including the U.S. Supreme Court and U.S. District Court for the Southern District of New York, which noted the language is so vague that “Alice in Wonderland has nothing on section 518.”

Then in 2018, a majority of the state Court of Appeals judges decided the state law is fulfilled "if and only if the merchant posts the total dollars-and-cents price charged to credit card users," which alleviates "concerns about luring or misleading customers by use of a low price available only for cash purchases."

Businesses can be fined up to $500 for each violation, asked to refund the amount not properly disclosed and potentially charged with a criminal misdemeanor — although courts are unlikely to impose such a serious penalty, according to Hack.

Most business owners that spoke with Newsday said they didn't realize that they were skirting the law by listing cash prices and posting signs stating that credit card users would be charged more.

'It gets kind of challenging ... There can't be any surprises.'

-Tayne Law Group founder Leslie Tayne

Credit: Tayne Law Group, P.C.

"It gets kind of challenging," said Tayne Law Group founder Leslie Tayne, who noted that merchants are also dealing with credit card network and issuer rules that may forbid surcharges, but allow them to pass off the cost if it's described as a convenience fee. "They all have to be disclosed no matter what. There can't be any surprises."

COVID-19 boosted card use

Many companies on the Island, particularly mom-and-pop operations, stopped absorbing swipe fees during the COVID-19 era, when running a business became more challenging, payment processing firms said.

Early in the pandemic, more customers avoided cash and used cards, which made the swipe fees a bigger burden, merchants said. And now, with skyrocketing inflation pushing up their other costs, even more businesses are transferring processing fees to consumers because they're one of the few expenses that can be curbed, payment processors said.

UpNexa, a Holbrook firm that processes payments for merchants, has seen a 60% increase in the number of companies passing on the fees since the pandemic began, said chief operating officer Jazzel Riquelmy.

"Before, it was like the deli and the bagel shops that were really interested in doing it,” said Riquelmy, of Mount Sinai. “We’ve seen a big influx from those with larger tickets: the restaurants, the medi spas — even down to churches and [private] schools.”

Anatomy of a swipe

Credit card transactions come with at least two fees. A fee averaging 1.3% to 3.3% of the transaction value is charged by the bank or institution that issued the credit card; and an average of 5 to 10 cents per transaction is collected by Visa, MasterCard or other networks used to transfer the money, according to The Motley Fool, a personal finance-focused publication.

Businesses often hire merchant processing firms to ensure everyone involved gets the proper fee — and their services also cost money, said Desh Singh, who launched CardEvo Inc., a Melville-based payment processing company, with his brother PJ Singh about four years ago.

“I’d say there’s five to 10 companies that are being paid out all at the same time for each transaction,” Singh said.

He estimated that before passing on the cost to customers, his Long Island clients paid an average of $1,050 a month in processing fees — an expense that has grown with the proliferation of credit cards that give people travel points, cash back or other rewards for charging purchases. These types of cards tend to have higher processing rates, according to The Motley Fool.

American businesses paid $105.2 billion in fees last year to accept credit card payments, according to the Nilson Report, which publishes updates on the card and mobile payment industry. That's 25% more than firms spent in 2020 and 50.8% more than they paid five years before that, Nilson said.

Merchants must also pay to accept payments via debit card, but the fees are lower because the federal government has capped them for about a decade. Still, many businesses subject debit and credit card users to the same fees because distinguishing between the two and treating them differently would be too complicated, Tayne said.

The industry draws from fee revenue to combat fraud and ensure networks can safely and quickly transfer money, according to the Electronic Payments Coalition, a trade group for credit card issuers and networks. The group's chairman Jeff Tassey said credit card rewards programs induce enough spending to benefit everyone, including small businesses.

An 'astronomical cost'

Swipe fees became too much for Capo Ristorante in Franklin Square during the pandemic, owner Paul Capoziello said. Processing costs were sometimes more than the restaurant's rent, he said. Demand for delivery skyrocketed and nearly all customers paid with plastic; today, about 87% do, Capoziello estimated.

A fire destroyed Capo's prior location and Capoziello tacked a 4% fee onto credit card bills when he reopened the restaurant in Franklin Square last year. Keeping a less expensive cash option for those on a budget seemed better than raising his prices across the board, Capoziello said. He said the shift went over fine with customers.

An example of a credit card surcharge on a receipt.

“Uber Eats, DoorDash — people choose to get deliveries of food from them, and they pay 30% more to get it delivered,” said Capoziello, of Franklin Square. “If they come in and get it or they’re ordering it from me, what’s another 4%?”

Melville Deli on Route 110 shut for two months in the early days of COVID-19 and then spent six months recovering from the closure, co-owner Simaan Gaffary said. With attendance at nearby offices down and food prices up, instituting a 3.5% surcharge on cards has helped the business save about $2,500 to $3,000 a month in fees, he said.

"That made the difference," said Gaffary, of Islip. "Before that we weren't making anything."

Signs on the deli's refrigerated displays announce a special offer of $12.95 for premade heros or $6.99 for half a sandwich — both of which are only relevant to customers with cash. On the front of the cash register, one sign notes the advertised prices reflect a cash discount and a second handwritten note says there will be "a 3.50% immediate discount on service charge" for those paying with cash or a gift card. Gaffary said he believed the setup met government standards, noting that it was approved by his merchant processor.

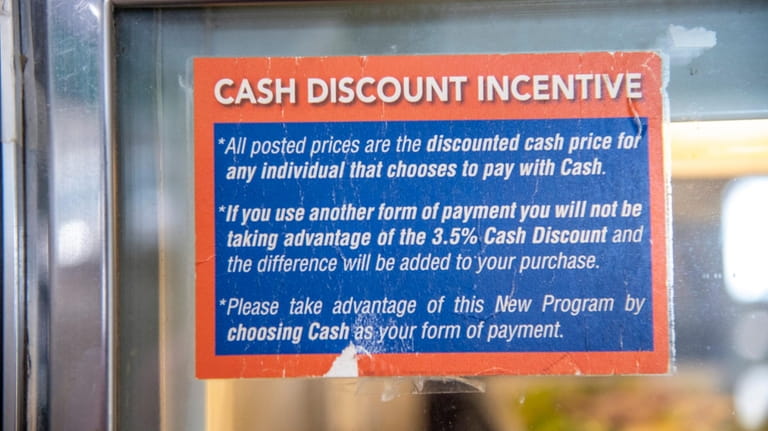

The "Cash Discount Incentive" sign inside the Bay Deli in Halesite on Wednesday, Oct. 19, 2022. More businesses are passing on the cost of processing credit card payments. Businesses are adding surcharges to the bills of those with cards and/or offering a discount to people paying with cash. Credit: Rick Kopstein

At Bay Deli in Halesite, owner Conrad Pohlmann instituted a card surcharge when a customer with payment processing experience suggested he do so. Pohlmann posted a sign near the register alerting customers that the advertised prices factor in a 3.5% discount for using cash. He now pays about $2,000 a year in processing costs, compared with $8,000, Pohlmann said.

"It's well worth it," said Pohlmann, who noted nobody has suggested his system doesn't meet state standards.

'It's well worth it.'

-Bay Deli owner Conrad Pohlmann, who instituted a card surcharge after a customer suggested it.

Credit: Rick Kopstein

At Signature Styles hair salon in Patchogue, owner Jean Bieselin is weighing whether to start splitting the processing payments with customers in 2023. The swipe fees she pays rose earlier this year, which helped push the salon’s monthly processing tab up to about $500, Bieselin said.

Her salon is facing other challenges, including having to buy products from Amazon because cheaper alternatives aren't available from wholesalers.

'It’s getting astronomical.'

-Signature Styles hair salon owner Jean Bieselin

Credit: Newsday/ John Paraskevas

“I took on a responsibility to pay a certain amount,” said Bieselin, of Patchogue. “It’s getting astronomical."

A common strategy

For small businesses, credit card processing fees have become a bigger concern under current economic conditions, Singh said. Firms are grappling with higher supply and labor costs and consumers tightening their budgets, he said. Many mom-and-pop enterprises can’t survive without cutting costs — and passing on these fees may be one of the few options at their disposal.

“They’re having to do this out of necessity to stay afloat," Singh said.

Nationwide, about 23% of small businesses use credit card surcharges, adding an average of 2.3% of the transaction value, according to a survey conducted by The Strawhecker Group, a payment consulting firm.

More Long Island firms are adopting this strategy as well, Singh said. Early in the pandemic, just a fraction of businesses working with CardEvo had consumers cover credit card fees, Singh said. Now nearly 90% of new clients opt for that model, he said.

Long Islanders have taken notice, with some saying they try to bring cash when eating out or running errands.

Jordan Hoffman, of Babylon, said he routinely informs businesses that their prices aren't properly displayed. Managers and owners respond that their system was OKd by a payment processor, he said.

If businesses give him a hard time, Hoffman notifies the attorney general's office. He's filed roughly 15 complaints with the office and seen two or three businesses reform their ways, said Hoffman, a real estate attorney.

Sharon Abrams, a retiree in Nassau County, said surcharges can be particularly shocking on big expenses.

Her husband died this summer, and Abrams worked with a funeral home to fulfill his request to have his body cremated. She was surprised to hear that using a card to cover the more than $1,375 service would come with a nearly $50 "convenience" fee. Abrams said she had no choice but to agree to the arrangement.

“I didn’t have liquid cash,” she said.

"When it happens in restaurants … most people are just like: eh, it stinks,” Abrams added. “When it is for something substantial, it can make a difference.”

Surcharges — even for smaller purchases — bother Debbie Jansen, of Great Neck.

She sympathizes with businesses that suffered during lockdowns, but noted that customers have also weathered tough spells.

“Many of us were unemployed for a long, long time and are thrilled to even be able to go out to eat,” said Jansen, who lost two jobs during the pandemic and works as an administrative receptionist.

Sarina Trangle covers affordability and cost of living issues and other business topics. She previously worked as an editor and reporter at amNewYork.

Updated 55 minutes ago Ex-LI man sets self on fire outside Trump trial ... EPA forever chemicals ... SCPD promotions ... Knicks preview

Updated 55 minutes ago Ex-LI man sets self on fire outside Trump trial ... EPA forever chemicals ... SCPD promotions ... Knicks preview